The 2025 U.S. budget deficit (Sept. fiscal yr.) narrowed by $41B to $1.775T, as $195B in tariff revenue and cuts to education spending (-$233B) helped offset higher outlays on healthcare and retirement programs and interest on the debt ($1.2T). While the ’25 budget deficit fell to 5.9% of GDP (vs. 6.3% in ’24), Treasury Secretary Bessent’s 3% target seems a long way off.

Ebbing systemic liquidity is beginning to expose malinvestment fostered by years of QE and ZIRP. In the wake of recent bankruptcies of auto-industry companies First Brands and Tricolor Holdings, investors punished regional banks on Thursday, with Zions Bancorp -12%, Western Alliance -11% and Jefferies -9%. The SPDR Regional Bank ETF declined 6.2%. As JPMorgan CEO Jamie Dimon noted earlier this week, “When you see one cockroach, there’s probably more.”

Goldman Sachs President John Waldron echoed Dimon’s concerns in noting the decade-long explosion to $5T of borrowings across high-yield bonds, leveraged loans and private credit. “We probably will have some defaults there, and it’s not going to be pretty when it happens.”

Euro Stoxx 50 -0.9%, S&P futures -0.4% and Nasdaq futures -0.55%. Spot gold -0.45% and spot silver 0.7%.

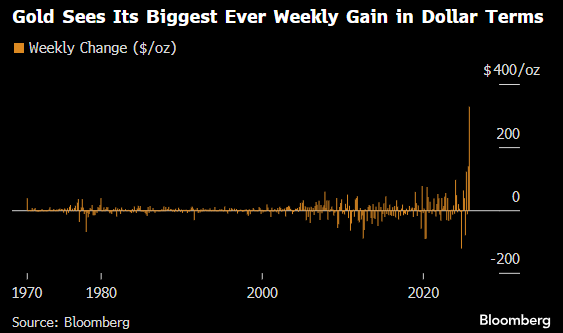

Chart of the week: After touching yet another all-time high ($4,380) in early Friday trading, spot gold’s 8% weekly gain is headed for its sharpest weekly percentage gain since March ’20. In dollar terms, spot gold’s weekly advance is now by far the largest on record.